I carried $80k in debt across seven credit cards for several years. COVID, family health problems, supporting people. I never missed a payment during that time. But I was paying roughly $1,400 every month in interest alone. I tried to make extra payments whenever I had spare cash, but I was guessing where to put the money. My total balance rarely moved.

Why Spreadsheets Failed for Seven Accounts

I'm a developer, so I started with Excel. I built a spreadsheet to track weighted average APR and model a payment schedule. It worked for basic tracking, but the logic fell apart once I tried to account for cards with multiple interest rates on the same account. Purchase APR on one portion, cash advance APR on another.

Maintaining the formulas became a secondary job. No version history, no easy way to cross-reference bank statements against projected balances. I went back and forth between Excel and .NET maybe three or four times before I committed. Eventually I built a personal tool in .NET with proper dashboards and charts so I could see month-by-month where every dollar was going.

What the .NET Charts Actually Showed

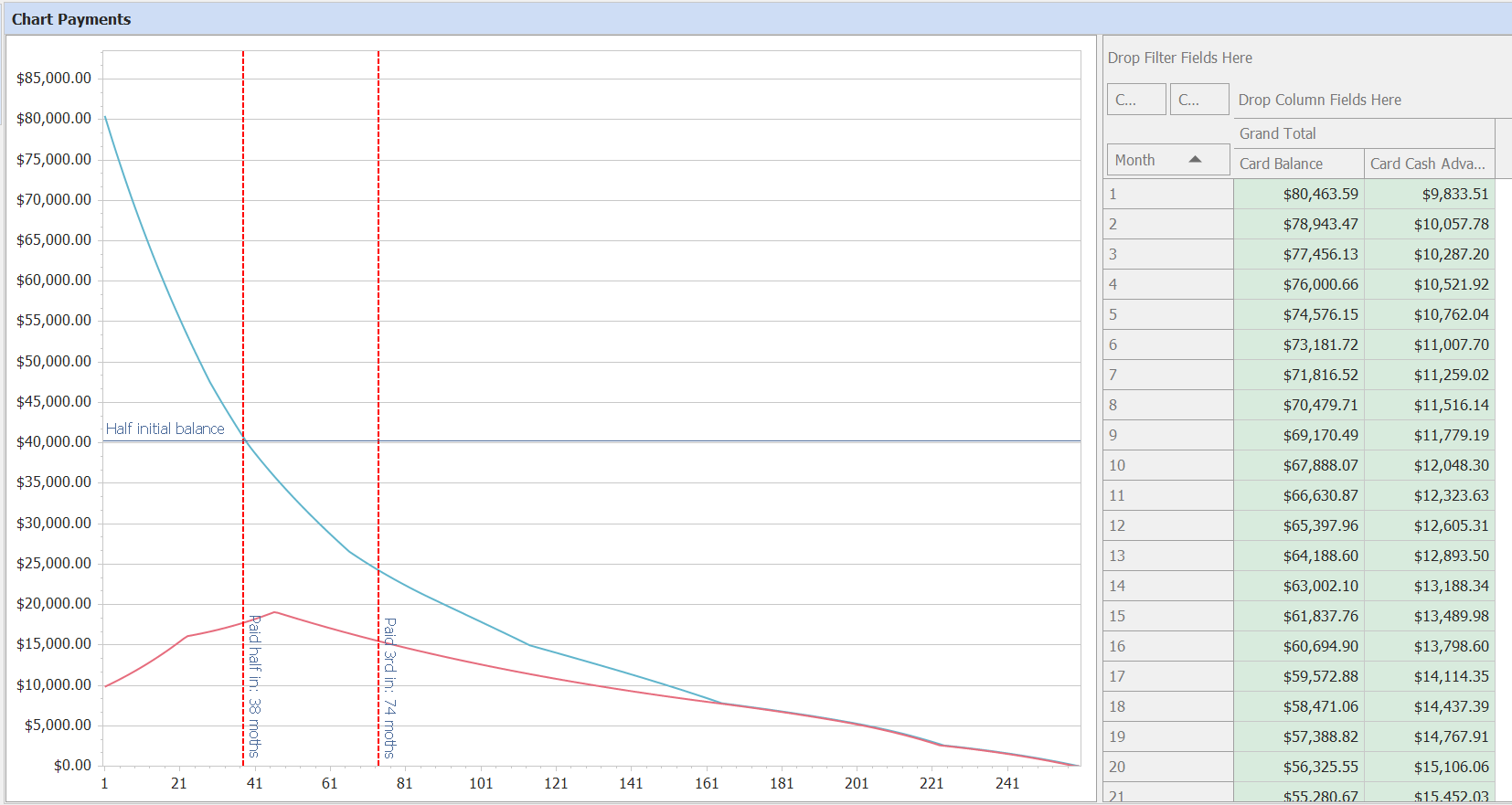

I built a chart to project my balances over time with just minimum payments. I assumed every balance would eventually trend down. The data showed something different. My total debt was decreasing slightly, but the cash advance balance was trending upward. That line went UP.

I had $9,800 in cash advance balances across two cards. One at 29.99% APR on a $5,000 balance, another at 24.99% on $4,800. That 29.99% segment alone was generating about $125 in interest every month. No grace period on cash advances, so interest compounds immediately. My minimum payment was barely covering it.

Understanding the CARD Act and Payment Allocation

I spent time going through my bank statements and reading about how payment allocation actually works. Under the CARD Act (specifically Regulation Z), banks have specific rules for applying your payments. When you pay more than the minimum, the excess goes to the highest-APR balance. That part is good.

The problem is the minimum payment itself. Banks generally apply your minimum to the lowest-APR balance first. I had low-interest purchase balances on the same cards as my high-interest cash advances. So my minimum payments were quietly paying off the cheap debt while the 29.99% balance sat there and grew. The two cards combined were generating about $245 in interest every single month just on cash advances. A few dollars toward the actual balance. Some months, not even that.

I ran the projection forward. Without action, the $9,800 would have taken over 25 years to pay off. I would have paid over $38,000 total. Nearly 4x the original amount. Most credit card payoff calculators miss this entirely because they treat each card as having one single interest rate.

Could your cash advance balance be growing too?

Senaro™ tracks Purchase APR and Cash Advance APR separately, so you can see what's really happening with your debt.

Check Your NumbersSwitching to the Avalanche Method

Once the math was visible, I stopped paying extra on random cards. I focused every extra dollar on the 29.99% cash advance. Tax return came in. A bonus. I put everything on that one balance. $1,500 one month. $4,350 the next. The cash advance went from $5,000 to zero in about two months.

Then I moved to the next highest rate. That's the debt avalanche method. You don't pay off the smallest card first for a quick win. You go after the card that's costing you the most in interest. For me, this shift saved approximately $100 per month in interest compared to my old approach of guessing. Over a year, that's $1,200 just by changing the order of payments.

The snowball method (smallest balance first) works too. Some people need the motivation of watching a card hit zero. Investopedia has a good comparison of the two approaches. Senaro™ shows you both strategies side by side with your actual numbers so you can see the dollar difference yourself.

What Every Credit Card Calculator Gets Wrong

I tried Mint for a while. It was useful for seeing where money went, but it didn't help me figure out how to pay it off faster. Every calculator I tried from NerdWallet, Bankrate, and Credit Karma treated each card as a single APR. None of them handled the things that were actually costing me money:

- How small extra payments ($10, $50, $100) change your total interest and payoff date across multiple cards with your exact numbers

- Separate Purchase APR from Cash Advance APR per card, which is what was invisibly growing my balance

- Avalanche vs Snowball comparison side by side showing the actual dollar difference, not just a generic explanation

- Month-by-month breakdown of where every dollar goes, principal vs interest, card by card

From .NET to a Private Web Tool

Senaro™ grew out of that personal .NET project. I wanted to make the tool available to others, but I didn't want to manage a database of sensitive financial data. I rebuilt the calculator as a static web app. HTML, CSS, and JavaScript. The math runs entirely in the browser. No financial data gets sent to a server.

Senaro™'s credit card payoff calculator handles all the details above. No signup, no bank linking. It saves to your browser's localStorage and stays on your device.

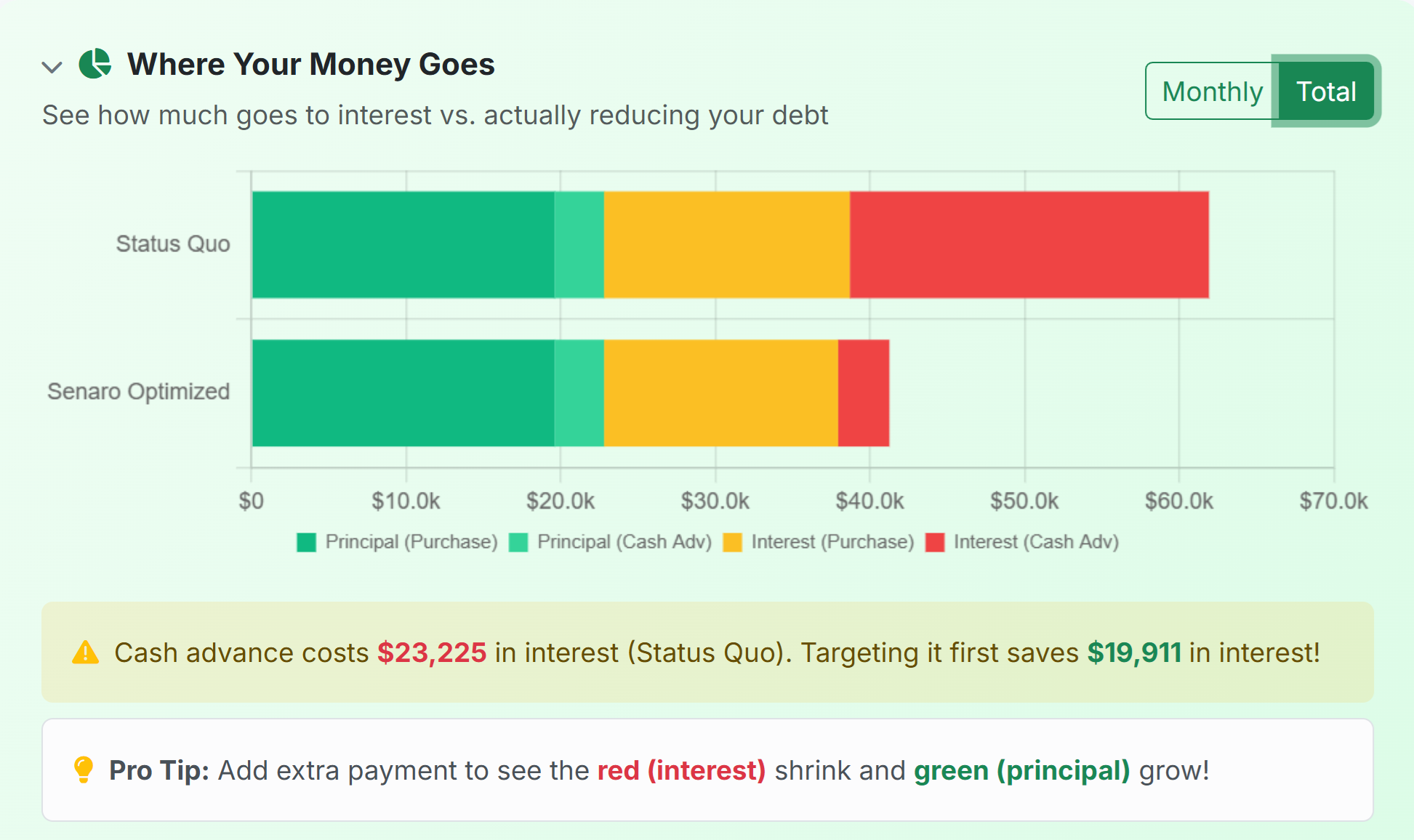

In this example: $32,500 across 5 cards (12.99%–29.99% APR), with $100/month extra toward payoff.

The Mistakes That Cost Me Real Money

Looking back, I made the same mistakes for years:

- Paying extra on random cards. Some months I'd throw $200 at my biggest balance, other months the card I just used. No math behind it.

- Assuming minimums attack the highest APR first. I knew about the 29.99% rate. I just assumed the bank would apply my payment there first. They don't. Under the CARD Act, minimums go to the lowest rate. I didn't check until the balance stopped moving.

- Only looking at total balance. My total was going down, so I thought I was making progress. One balance was growing while I made payments on everything else.

- Thinking $50 extra doesn't matter on $80k. On a 29.99% card, $50 extra per month cuts years off the payoff timeline.

I have paid off roughly half of my original $80k balance since I started using the data to drive my decisions. My income didn't change significantly. I just stopped guessing where to put the money.

I'm building Pro features. Smarter payoff strategies, what-if scenarios, PDF exports.

Get notified when Pro launchesWhat's Next

Right now Senaro™ is a free calculator. Pure math, runs locally. I'm working on adding what-if scenarios, progress tracking, and smarter payoff recommendations. The core calculator will stay free.

Try the Free Credit Card Payoff Calculator

See your real debt-free date. Enter your cards, compare avalanche vs snowball, and see exactly where every dollar is going.

Free forever. No signup. 100% private.

Written by Alex

Software developer who built Senaro™ after managing $80k in credit card debt across 7 cards. The calculator started as a personal .NET tool before becoming a free web app. Built in 2026.